Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

What a cup of coffee taught me about Black-Scholes, CAPM, and the limits of financial models. Models simplify reality - but reality complicates models.

In finance, we rely on elegant equations to make sense of messy reality. Strangely enough, my morning coffee reminded me just how fragile those equations can be.

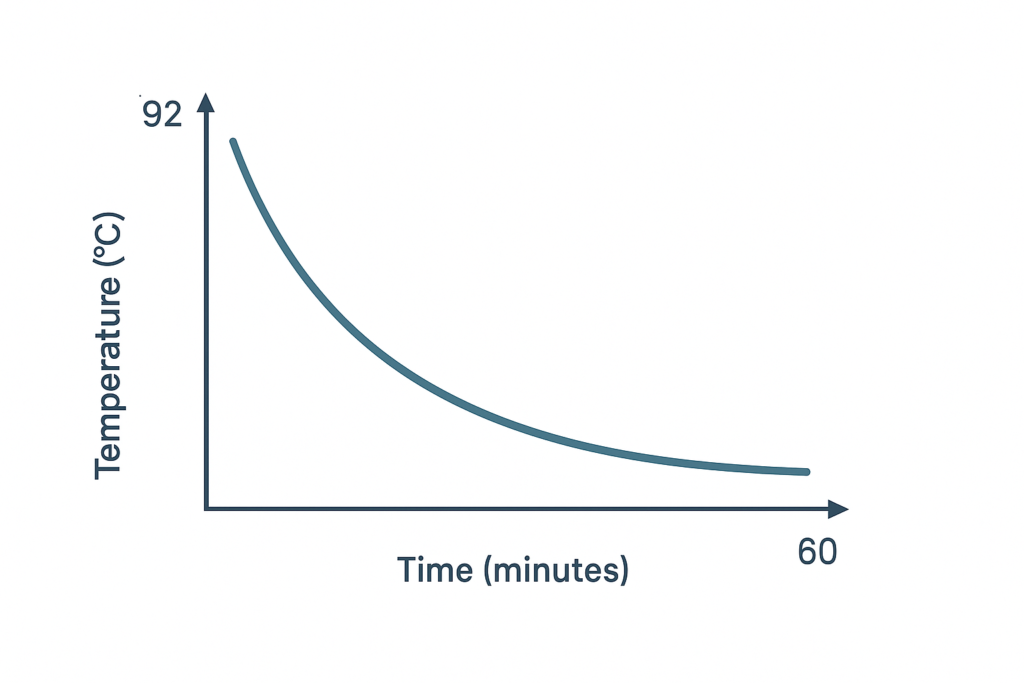

This morning, I brewed a fresh cup of coffee and instead of just waiting, I asked myself: “How long will it take before this is drinkable?”

Being me, I thought let ‘s reach for calculus to solve this.

I treated the coffee like a textbook exponential decay problem:

With a simple first-order differential equation (Newton’s Law of Cooling), the math told me: about 11 minutes until sip ready.

What if I added milk?

What if I stirred the coffee?

What if I covered it with a lid?

What if the mug was twice as big or made of metal instead of ceramic?

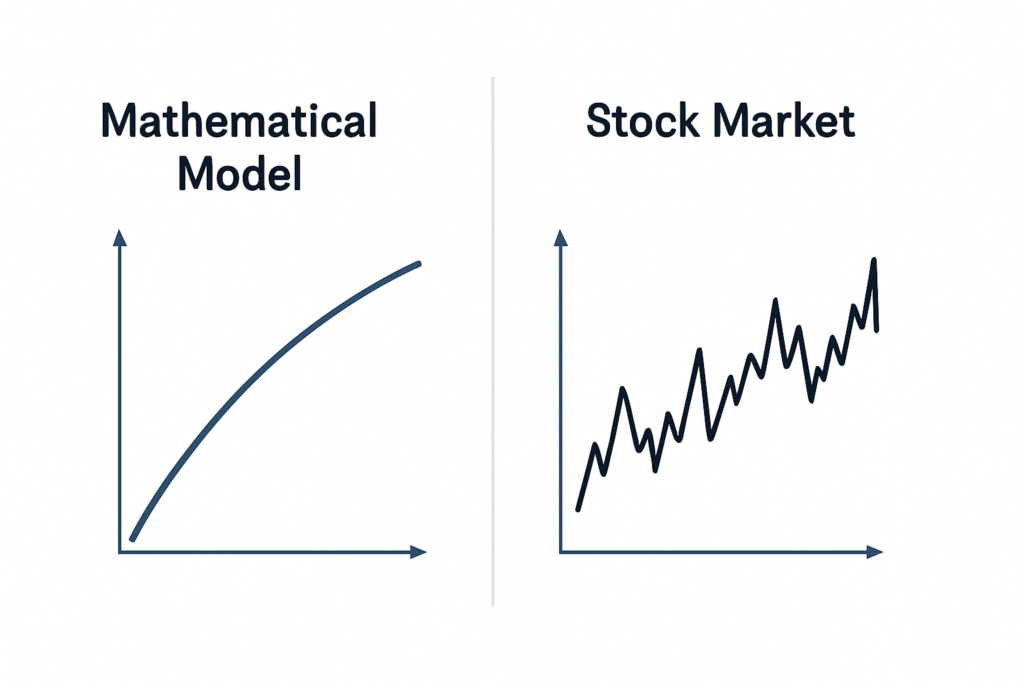

Finance is full of beautifully elegant models, as neat as my cooling-curve equation

And just like coffee, reality doesn’t play along:

“In practice, it’s not just about knowing the model, it’s about knowing when the model is lying to you.”

My coffee reached sip zone in about 11 minutes, give or take. But the bigger takeaway wasn’t about caffeine.

It was this:

Models simplify reality. Reality complicates models. Knowing the difference is expertise.

Sometimes, the best reminder of that truth is right in front of us – in a white ceramic mug.